Read our latest Insights article on the newly updated Fuel Tax Credits rates now in effect via the link (blog.agredshaw.com.au)

For businesses managing a vehicle fleet, the Fuel Tax Credits system can be an excellent route for operators to claim full or partial credits for the fuel tax (excise or customs duty) that’s included in the price of fuel.

Under the FTC system, fuel used in machinery, plant & equipment, heavy vehicles, and light vehicles over 4.5 tonnes gross vehicle mass travelling off public roads or on private roads can be entitled to a certain rate of credit dependent on when you acquire the fuel, what it is used for, type of fuel, and the business activity for its use.

Fuel Tax Credits are claimed on your Business Activity Statement, and you may make a claim within four years of purchasing the fuel. The amount of credit changes every six-months (February & August) and in-line with February CPI index factors, Fuel Tax Credits have now increased by 1.009 until 30 June 2021.

What types of vehicles & fuel types are eligible to claim the Fuel Tax Credits?

We have included an outline of eligible vehicles, suitable to claim the Fuel Tax Credits:

- concrete transportation vehicles;

- refrigerated vehicles;

- waste management collection vehicles;

- long-haul vehicles with sleeper cabins;

- vehicles with specialist auxiliary equipment (ie. trucks with equipment for unloading/loading, elevated work platforms, truck-mounted loader cranes, drilling equipment, pumping equipment, and truck-blower for dry good).

Additionally, we have also included a list of eligible fuel types which can be claimed:

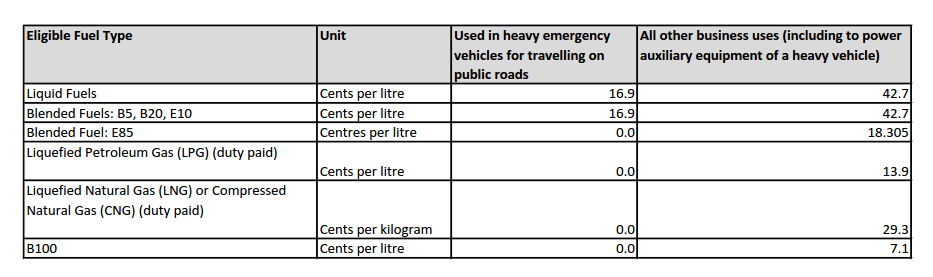

- Liquid fuels (for example - Diesel or Petrol);

- Blended fuels (B5, B20, E10);

- Liquefied Petroleum Gas (LPG) (duty paid);

- Liquefied Natural Gas (LNG) or Compressed Natural Gas (CNG) (duty paid);

- Blended fuel (E85)

- B100

The updated Fuel Tax Credit rates are as follows (per the ATO website):

What records are required to claim Fuel Tax Credits?

Businesses must keep a detailed motor vehicle logbook for a five-year period - containing the following information:

- when the logbook period begins and ends;

- date of each trip;

- odometer reading at the start and end of each trip;

- kilometer travelled per trip and reason travelled;

- the total business use percentage in the logbook;

- odometer readings for the start and end of each Income Tax Year that you use the logbook

Further information on the records you need to provide are outlined below:

| Information your records need to show | Examples of types of records |

|

|

You will need to keep more than one of these record types to support your claims. For example, you will need to keep tax invoices to show when you acquired the fuel, copies of contracts to show the activities that the fuel was used in, as well as GPS data if some of your fuel is used in a heavy vehicle that operates off a public road.

Are there other eligible areas vehicles can claim Fuel Tax Credits?

Heavy vehicle operators may be eligible to claim further tax credits for fuel used to power auxiliary vehicle equipment. This eligibility is subject to select criteria surrounding fuel types and applied to heavy vehicles (including emergency vehicles) with a gross vehicle mass greater than 4.5 tonnes.

It is important to note that fuel used to power the auxiliary equipment may be sourced from a separate fuel tank or from the tank that fuels the main engine. Additionally, the auxiliary equipment may also take its power from the main engine, which in turn increases the fuel used.

Additionally, where you have a non-heavy vehicle that is used both on-road and off-road you will need to estimate the percentage that is off-road and only claim that amount. This includes if you are travelling between properties on a public road.

For More Information

For more information on your eligibility to claim additional Fuel Tax Credits or an initial consultation, please contact Smiljan Jankovic, Managing Director - Archer Gowland Redshaw, on (07) 3002 2699.

Disclaimer

The information contained in this article is of a general nature and does not take into account personal circumstances. Before making any decisions based on the factual information contained in this document, please consult with your financial adviser.